Over the past week, Russia rejected Ukrainian sovereignty, formally recognized the separatist regions of Luhansk and Donetsk, sent troops there, and then a day later invaded the entire country. Russian aggression and the declaration of war signals a rupture to the post-Cold War political order in Eastern Europe, and it could have devastating effects on Ukrainian civilians and the Ukrainian and Russian economies. But the war itself is not surprising.

For weeks, the U.S. government has been warning that a Russian invasion was imminent, and it finally arrived this week. Markets have been pricing in this possibility for some time.Market volatility leading up to this moment has been normal from a historical perspective—geopolitical crises and regional conflicts tend to hurt sentiment, create short-term uncertainty, and drive volatility. Looking back at 54 crisis events since 1907, the Dow Jones Industrial Average has fallen an average of -7.1% during the crisis period, according to global investment research firm Ned Davis Research.

The Dow gained an average of +9.7% in the six months following a crisis

But stocks also tend to bounce back once the actual fighting breaks out. The same research from Ned Davis shows that the Dow gained an average of +9.7% in the six months following a crisis. Similarly, data compiled by BMO shows that the S&P 500 has averaged an +8% return in the 12-months after a geopolitical conflict commences. The fact that stocks rallied on the day of the Russian invasion is not that surprising.

We also know that looking back at conflicts since 1925 (when reliable S&P 500 data became available)—the Korean War, Vietnam, the Cuban Missile Crisis, the Iran/Iraq War, two U.S. wars in Iraq, the list goes on and on—it was only World War II that resulted in a bear . Some readers may even recall that when Russia invaded and annexed Crimea in 2014, the S&P 500 continued to move higher, and did so for years:

Source: Federal Reserve Bank of St. Louis

The point here is not that armed conflict is bullish. The point is that uncertaintyleading up to a conflict is what tends to weigh on markets. Once the conflict is averted or fighting breaks out, the uncertainty fades and markets can start to price in the effects on corporate earnings, financial markets, and global economic growth.

In this case, Ukraine’s GDP makes up just 0.2% of the world’s total, and the country’s investable market is comprised of just two companies. This war is likely to be devastating in many ways, but the bottom line is that Ukraine – and the other former Soviet states that could get drawn into the conflict from here – are simply not big enough to cause a ripple in the global economy.

Russia is of course a different story. The Russian economy makes up just 2% of global GDP, but the country is the world’s third-largest oil producer (the United States is the largest, followed by Saudi Arabia), and it is the world’s largest exporter of natural gas. Russia is also a major producer of wheat, aluminum, nickel, and other metals.

During a time when oil, gas, and metals markets are experiencing tight supplies and firm demand, disruptions to Russian output could drive up prices and particularly impact countries that rely heavily on Russian exports.

It makes sense to remain overweight U.S. equities

The United States is not one of them. Russia and Ukraine combined makeup far less than 1% of total U.S. imports and exports, and Russia’s status as a major natural gas exporter does not affect the U.S., given the U.S. is also a net exporter of natural gas.

In an optimistic scenario, reduced oil and gas flows from Russia could ultimately present an opportunity for U.S. oil and natural gas producers to extract and export more, becoming an even more influential player in global commodities markets.

Regardless, additional near-term pressure on oil prices appears likely, but the effect on the global economy and markets may not be as drastic as many people fear. An analysis from Goldman Sachs finds that a $10 per barrel increase in the price of oil would boost U.S. headline inflation by 0.20% while lowering GDP growth by just 0.1%.

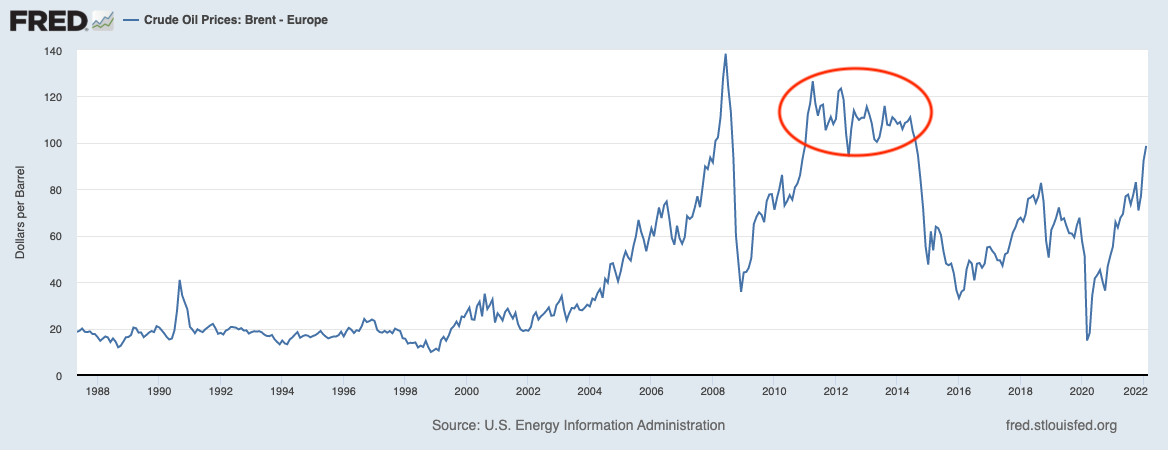

It is also worth remembering that oil prices (chart below) remained firmly above $100 a barrel from the beginning of 2011 through the summer of 2014, during which time the U.S. economy grew and the stock market went up by over +50%. Higher oil prices do not necessarily mean economic recession or weak markets.

Source: Federal Reserve Bank of St. Louis

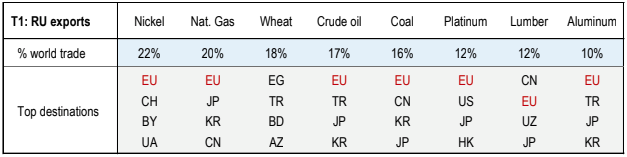

The European Union is more exposed as a result of this conflict. Russia supplies some 40% of Europe’s gas, and the EU also relies heavily on other commodity exports from Russia (see table).

Source: Numera Analytics

Vladimir Putin has stated that gas and other commodity exports will continue to flow, but the realities of war may ultimately affect supply in the coming months. We believe it makes sense to remain overweight U.S. equities.

All of these factors are important when weighing the outlook for global economic growth. But a recession requires trillions of dollars’ worth of damage to the global economy, which Russia and Ukraine are simply not capable of delivering. After all, S&P 500 companies have only a very small fraction of 1% of revenue and profit exposure to Russia and Ukraine combined.

Fearful headlines will flood the internet

Western countries have been united in condemning Russian aggression, and the U.S., U.K., Australia, Japan, and the European Union have all already issued a ‘first tranche’ of sanctions. Notably, Germany has halted the approval process for the Nord Stream 2 gas pipeline to become operational, in a largely unexpected move. More severe sanctions are planned from here.

Market volatility is likely to continue as the conflict escalates and sanctions (and economic retaliation from Russia) come into view. News coverage will be constant and fearful headlines will flood the internet and perhaps your phone and your inbox. Investors should brace for this outcome now, and try to remember that the desire to react to the crisis is almost always counterproductive and costly.

Ein persönlicher Nachtrag: Am Donnerstag hat der S&P 500 die Marke von -15% vom Hoch (rund 4.100 Punkte) knapp erreicht. An dem Punkt wollte ich wiederum nachkaufen. Das habe ich auch getan – am Freitag. Die Position in PAYPAL habe ich aufgestockt, die in ETSY und PINTEREST ebenfalls. Ob damit die Korrektur beendet ist? Who knows! Fällt der Markt weiter, kaufe ich bei -20% vom Hoch (3.850 Punkte im S&P 500) wiederum nach.

Wenn du keinen Beitrag mehr verpassen willst, dann bestell doch einfach den Newsletter! So wirst du jedes Mal informiert, wenn ein neuer Beitrag erscheint!